By Steven Johnson, DBA, CPA, CITP and Byron Pike, PhD, CPA

One of the most challenging issues facing leaders in the public accounting profession is the high rate of employee turnover. A recent survey finds that turnover in large CPA firms (those with revenues in excess of $75 million) is 17%, and one in every six firms experiences annual turnover of 20% or greater (Inside Public Accounting National Benchmarking Report, Platt Consulting Group, 2015). Given that the direct costs associated with replacing a professional staff member can be as much as 50%–60% of the employee’s annual salary, there is little wonder why firms are continuously searching for ways to keep high-quality employees (Terence Mitchell, Brooks Holtom, and Thomas Lee, “How to Keep Your Best Employees: Developing an Effective Retention Policy,” Academy of Management Executive, November 2001, https://bit.ly/2yUU2Zv).

Employee satisfaction has received considerable attention as companies attempt to improve employee retention. In fact, many organizations ask employees to take annual surveys to determine overall satisfaction, with the goal of targeting areas for improvement. While this is certainly a noble effort, focusing on employee engagement could represent a more effective method for not only improving employee retention, but also increasing productivity.

Many large corporations devote substantial effort to measuring and improving the engagement of their employees; CPA firms, however, have generally given little attention to this. Because employee engagement is not a one-size-fits-all solution for improving employee retention and performance, it is important to measure the engagement of employees within CPA firms. The authors surveyed a cross-section of CPA firm employees to determine the extent of their engagement. Moreover, the authors used the obtained data to identify the factors that have the greatest impact on employee engagement at CPA firms. Based on these findings, the authors provide recommendations for how CPA firms can improve the engagement of their employees, which can lead to greater employee retention and productivity.

What is Employee Engagement?

Within the academic literature, employee engagement (also referred to as “work engagement”) has varying definitions. One of the most common definitions describes employee engagement as “an individual’s sense of purpose and focused energy, evident to others in the display of personal initiative, adaptability, effort, and persistence directed toward organizational goals” (William Macey, Benjamin Schneider, Karen Barbera, and Scott Young, Employee Engagement: Tools for Analysis, Practice, and Competitive Advantage, Wiley-Blackwell, 2009). This description places emphasis on an individual’s “state of mind” while at work and is much different from employee satisfaction, which generally measures an employee’s level of contentment with the work environment.

To illustrate this point, satisfaction is nearly always measured by a single question in an employee survey: “How satisfied are you with your job?” Conversely, engagement is quantified using multiple questions that attempt to measure an individual’s state of mind and emphasize items relating to enthusiasm, pride, passion, focus, and energy on the job.

Research consistently finds a significant relationship between employee engagement and positive outcomes within organizations. Specifically, empirical evidence suggests that employee engagement has a direct effect on job performance, return on assets, customer loyalty, profitability, and reduced employee turnover (Michael Christian and Jerel Slaughter, “Work Engagement: A Meta-analytic Review and Directions for Research in an Emerging Area,” Academy of Management Annual Meeting Proceedings, August 2007, https://bit.ly/2APGEY0; James Harter, Frank Schmidt, and Theodore Hayes, “Business Unit–Level Relationship between Employee Satisfaction, Work Engagement, and Business Outcomes: A Meta-analysis,” Journal of Applied Psychology, May 2002, https://bit.ly/2qwBESn). Thus, employee engagement is a more inclusive construct that can translate into greater employee retention, as well as better job performance and profitability.

Research Methodology

The authors evaluated the extent of employee engagement in public accounting firms by surveying 1,064 employees across five different CPA firms in the Midwest. The survey focused on employee engagement, employee satisfaction, the employee’s intention to stay in the organization, and additional workplace variables. It was completed by 775 employees (72.8% completion rate).

Employee satisfaction was measured using the single question, “Overall, how satisfied are you with your job?” Employee engagement was measured using seven questions modeled after the Utrecht Work Engagement Scale (Willmar Schaufeli and Arnold Bakker, Utrecht Work Engagement Scale: Preliminary Manual, November 2003, https://bit.ly/2yVNxG5). This composite measure of employee engagement included questions such as, “I am enthusiastic about my job,” “I feel full of energy when I’m at work,” and “I am passionate about the work I do.” Intention to stay in the organization was measured by asking how likely it was that the employee would be working at the firm in one (short-term) and five (long-term) years. All questions were measured on a seven-point scale, with 7 being “strongly agree,” 1 being “strongly disagree,” and 4 being neutral.

Results

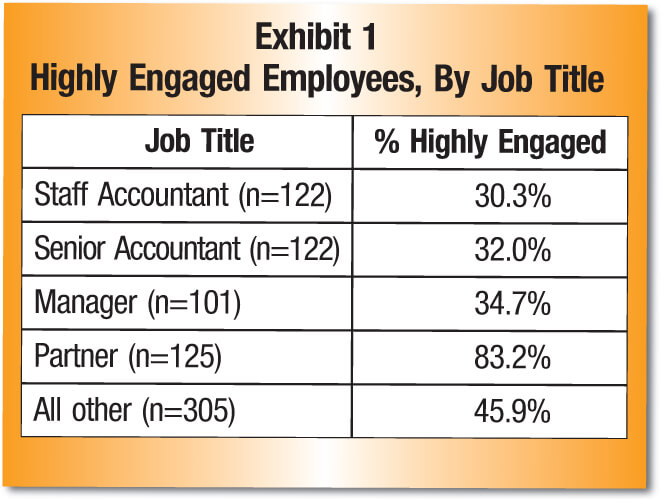

The survey results indicate that 45.8% of all employees in the public accounting firms surveyed are “highly engaged” (defined as an engagement score of 5.5 or greater). This level of engagement is consistent with most estimates of employee engagement in the general workforce. The authors further examined the participants’ engagement by segmenting the results based on the participant’s job title.

Exhibit 1 provides the engagement results by job title, illustrating a divide in engagement between groups of employees. Employees in staff, senior, and manager positions have significantly lower levels of engagement, with less than 35% classified as highly engaged. On the other hand, employee engagement by partners is dramatically higher than all other positions within the firms. If one views the employee engagement results based on the typical life cycle within CPA firms, high turnover in the public accounting profession is made salient based on the lack of engagement by lower-level staff members.

Because of the retention issue faced by most CPA firms, the study went beyond the measurement of employee engagement and examined its influence on an employee’s intention to stay in the firm (an indicator of actual retention). Based on the findings, employee retention is highly influenced by employee engagement, whereby highly engaged employees report a greater propensity to stay at their firm in both the short and long term. In fact, the level of engagement was the primary predictor of whether employees intended to stay in their organizations, accounting for over 40% of the differences in employees’ short- and long-term intentions to stay in the firm. While employee satisfaction can influence employee retention within CPA firms, engagement appears to be more important to an employee’s intention to stay in a firm.

The authors also performed a regression analysis to determine the factors that have the greatest impact on employee engagement. In many cases, organizations that conduct employee surveys have a tendency to only focus attention on the areas that receive lower scores, reasoning that every low score has a negative impact on engagement or the attribute being measured. The problem with this approach is that it treats all variables (or survey questions) as though they have an equal impact on the desired outcome.

For example, assume that a firm conducts an engagement survey and the question, “I have sufficient time to complete my job responsibilities,” receives very low scores. One reaction might be to create action plans to address this question, along with all other low scores from the survey. In reality, some lower scores are inconsequential because they have very little impact on employee engagement. Thus, it is important to focus improvement plans on the factors that have the greatest impact on employee engagement as opposed to using measurement scores alone to drive decision-making. The most effective means of determining what actually affects engagement is through the use of a regression analysis. This method removes the guesswork from improving employee engagement and provides the greatest return on investment, as resources can be allocated more specifically and effectively.

The authors’ regression analysis indicates there are three factors that have the greatest impact on employee engagement, accounting for over 65% of the differences in employee engagement from the surveyed CPA firm employees. (These primary drivers of engagement at CPA firms are presented in Exhibit 2.) Focusing on these three variables gives firms the best opportunity to enhance employee engagement, thereby improving employees’ intention to stay in the organization. Further discussion of each of these variables, along with specific suggestions for improvement, is provided below.

My job gives me the opportunity to do what I do best.

Job fit—whether one believes their skills are well matched to their responsibilities—surfaces time and time again as a driver of engagement across many different sectors and industries. This intuitively makes sense, as one would expect that an individual who feels as though his skills are being fully employed would also be more engaged in his job. Examples of successful approaches to improving job fit in firms include the following:

- Having specific conversations with employees about the job duties that they find fit best with their skills. Although potentially challenging at first, given continued attention, employees will begin to learn and discuss the areas of their job that best fit their skill sets. The goal is having the right people, in the right places, doing the right things.

- Making sure that career paths allow for job fit. Even though most organizations understand that the best sales person does not always make the best sales manager, such situations are frequently created. In public accounting firms, one of the most challenging issues is how to reward individuals who wish to stay in managerial roles and are not interested in moving to a partner role. Having a career path for these types of situations can help individuals stay in a role that provides them with the best job fit.

I believe my personal values are aligned with my firm’s values.

Value alignment within accounting firms can encompass a wide variety of different issues; however, this statement generally refers to firm culture and core values. Suggestions for improving this area include the following:

- Making sure to discuss and define the firm’s core values. In many cases, the discussion around core values is even more valuable than the actual establishment of them, as it provides all employees with an opportunity to provide input on the kind of firm for which they want to work.

- Being strategic in the hiring process. Creating a list of core values is important, but using them frequently to ensure that incoming employees’ values align with the firm’s values is just as important.

I believe I make a difference at work.

Interestingly, this driver is near the top of the list for millennials in many public accounting firms. There is an increasingly important desire for younger employees to believe that their work is making a difference in others’ lives. This satisfaction can come in a variety of different ways, but methods for improving this driver of engagement include the following:

- Making sure that the firm is telling its story, and telling it often. In many cases, accounting firms underestimate the positive impact they have on individuals’ lives; telling those stories can have a tremendous influence on helping employees understand the important role they play in those lives. In addition, it creates a common theme that can be shared not only with employees but also with current and prospective clients.

- Telling employees that they’re making a difference and celebrating those successes. With the multitude of demands placed on firms, it can be challenging to change the perspective in order to communicate individual and team success stories; however, doing so can have a profound impact on employees and engagement.

Building a Better Firm

Given the challenges of employee retention in public accounting firms, it is no wonder that firms are eager to explore ways to improve employees’ intention to stay with the firm. This study provides evidence that employee engagement is a primary contributor to employee retention, more so than the traditional emphasis on employee satisfaction. Although the guidelines listed above provide sound generalizations for improving engagement, all accounting firms are different. Most firms have areas—whether departments, locations, or job titles—that need more attention than others. Using a valid, reliable instrument to measure engagement can provide an effective means to create action plans for improving engagement across these different areas of the firm. This approach can not only improve employee engagement, but also lead to positive changes in employee retention, customer loyalty, and overall firm profitability.

Originally published on CPA Journal.